You use this program to maintain depreciation codes that establish the actual percentage rates of depreciation applied to an asset.

Depreciation codes can be applied to all depreciation books (i.e. Book value, Tax value and all Alternate valuations) in the Assets program.

- Asset Depreciation Code Details

- Asset Depreciation Varying Annually

- Asset Depreciation Varying by Period

- Depreciation Type Examples

| Field | Description | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Asset depreciation code | Indicate the depreciation code to maintain. | ||||||||||||||||||||

| Depreciation code | This indicates the depreciation code being maintained. | ||||||||||||||||||||

| Depreciation code information | |||||||||||||||||||||

| Description | This indicates the descritpion of the depreciation code. | ||||||||||||||||||||

| Depreciation type | Indicate the depreciation method to use for the

depreciation code. Refer to Depreciation Type Examples for calculation examples of the various depreciation types.

|

||||||||||||||||||||

| Varying depreciation | This only applies to Straight line

and Reducing balance depreciation

types.

|

||||||||||||||||||||

| Varying depreciation anniversary | This only applies when the depreciation code uses

varying depreciation. This does not apply when Varying depreciation is By period.

|

||||||||||||||||||||

| Annual depreciation % |

Indicate the annual depreciation percentage to use when not using varying depreciation (i.e. when Varying depreciation is No). This can only be greater than 100% for Declining bal with switch and Declining bal without switch depreciation types. This only applies to Straight line, Reducing balance, Declining bal with switch and Declining bal without switch depreciation types. |

||||||||||||||||||||

| Number of periods EUL |

Indicate the default life of the asset in periods. This only applies to Fixed EUL and Rem value over rem life depreciation types. The value you enter here is not fixed for this depreciation code as it can be changed against the depreciation book using the Assets program. It is merely the default value displayed when you select this depreciation code for a depreciation book (Assets). |

||||||||||||||||||||

| Number of years EUL | Enter the default fixed number of years over which the

asset must be depreciated. This only applies for the Sum of year digits and Declining balance with or without switch depreciation types. The value you enter here is not fixed for this depreciation code as it can be changed against the depreciation book using the Assets program. It is merely the default value displayed when you select this depreciation code for a depreciation book (Assets). |

||||||||||||||||||||

| Statistical G/L code |

Indicate the General Ledger code to which the statistical throughput value for the current period must be posted. This ledger code must have an Account type of Statistical (General Ledger Codes). The through-put value you enter in this statistical ledger code is used by the Asset Depreciation Calculation program when calculating the depreciation value for the asset for the current period. For this reason, you would create a unique statistical ledger code for each asset for which you want to calculate depreciation based on Statistical EUL. For example, if you are depreciating a vehicle based on throughput of kilometers, then for each period, you will enter the kilometres travelled for that period in the statistical ledger code you define here. This field is only enabled if you entered a Statistical EUL depreciation code type at the Depreciation type field. The value you enter here is not fixed for this depreciation code as it can be changed against the depreciation book using the Assets program. It is merely the default value displayed when you select this depreciation code for a depreciation book (Assets). |

||||||||||||||||||||

| Throughput EUL |

When you select the Statistical EUL depreciation method, you use this field to indicate the throughput Estimated Useful Life of the asset. This throughput could for example be the total mileage for a vehicle or the total number of copies in the life of a photocopier. The value you enter here is not fixed for this depreciation code as it can be changed against the depreciation book using the Assets program. It is merely the default value displayed when you select this depreciation code for a depreciation book (Assets). |

||||||||||||||||||||

| Apply half year rule | Select this to deduct 50% of the usual depreciation rate for any depreciable asset bought after the first period of the fiscal year. The usual rate is used to calculate depreciation for the subsequent years. This applies when your nationality is set to Canada. |

||||||||||||||||||||

| Date convention | This option only applies when your Date

conventions are set to Depreciation

code (Assets Register Setup).

|

||||||||||||||||||||

This listview enables you to indicate the annual depreciation percentages by which an asset book must be depreciated.

This listview is enabled when you select the Varying depreciation > Annually option.

| Field | Description |

|---|---|

| Year | This indicates the year number. |

| Percent | Indicate the percentage by which the asset must

depreciate in the corresponding year. For Straight line depreciation, the total of this column must add up to 100. |

This listview enables you to maintain the depreciation percentages by which an asset book must be depreciated in each period of the corresponding year.

This listview is enabled when you select the Varying depreciation > By period or the Varying depreciation > By period (fixed property) option.

| Field | Description |

|---|---|

| Year | This indicates the year number. |

| Period 1 - 13 |

Indicate the percentage by which the asset must depreciate in the corresponding period. For Straight line depreciation By period, the total of all the percentages entered must equal 100 (i.e.the totals for the entire grid must equal 100%). For Straight line depreciation By period(fixed property), the total of the percentages in each Period column must equal 100. |

This section includes examples of how depreciation is calculated for the various depreciation types.

![[Note]](images/note.png)

|

|

|

All examples are based on a 12 accounting periods (Company Setup). |

|

Asset cost = 120 000

Depreciation percentage = 10%

Years 1-10:

Annual depreciation = 120 000 * 10% = 12 000

Monthly depreciation = 12 000 / 12 = 1 000

Asset cost = 120 000

Depreciation percentage year 1 = 20%

Depreciation percentage year 1 = 40%

Depreciation percentage year 1 = 30%

Depreciation percentage year 1 = 10%

Year 1:

Annual depreciation = 120 000 * 20% = 24 000

Monthly depreciation = 24 000 / 12 = 2 000

Year 2:

Annual depreciation = 120 000 * 40% = 48 000

Monthly depreciation = 48 000 / 12 = 4 000

Year 3:

Annual depreciation = 120 000 * 30% = 36 000

Monthly depreciation = 36 000 / 12 = 3 000

Year 4:

Annual depreciation = 120 000 * 10% = 12 000

Monthly depreciation = 12 000 / 12 = 1 000

Asset cost = 120 000

Depreciation percentage per period per annum:

| Periods | Year 1 | Year2 |

|---|---|---|

| 1 | 1% | 1% |

| 2 | 2% | 2% |

| 3 | 2% | 3% |

| 4 | 2% | 4% |

| 5 | 2% | 5% |

| 6 | 2% | 6% |

| 7 | 2% | 7% |

| 8 | 2% | 8% |

| 9 | 2% | 9% |

| 10 | 2% | 10% |

| 11 | 2% | 11% |

| 12 | 1% | 12% |

Year 1:

Monthly depreciation:

This is calculated as Asset cost * depreciation percentage for each period.

I.e. Period 1: 120 000 * 1% = 1 200, Period 2: 120 000 * 2% = 2 400, etc.

The resulting monthly depreciation is as follows:

| Periods | Year 1 |

|---|---|

| 1 | 1 200 |

| 2 | 2 400 |

| 3 | 2 400 |

| 4 | 2 400 |

| 5 | 2 400 |

| 6 | 2 400 |

| 7 | 2 400 |

| 8 | 2 400 |

| 9 | 2 400 |

| 10 | 2 400 |

| 11 | 2 400 |

| 12 | 1 200 |

Annual depreciation:

This is the sum of all monthly depreciation values for year 1 = 26 400

Year 2:

This is calculated as Asset cost * depreciation percentage for each period.

I.e. Period 1: 120 000 * 1% = 1 200, Period 2: 120 000 * 2% - 2 400, Period 3: 120 000 * 3% = 3 600, Period 4: 120 000 * 4% = 4 800, etc.

The resulting monthly depreciation is as follows:

| Periods | Year 2 |

|---|---|

| 1 | 1 200 |

| 2 | 2 400 |

| 3 | 3 600 |

| 4 | 4 800 |

| 5 | 6 000 |

| 6 | 7 200 |

| 7 | 8 400 |

| 8 | 9 600 |

| 9 | 10 800 |

| 10 | 12 000 |

| 11 | 13 200 |

| 12 | 14 400 |

Annual depreciation:

This is the sum of all monthly depreciation values for year 2 = 93 600

Asset cost = 120 000

Depreciation percentage = 40%

Year 1:

Annual depreciation: 120 000 * 40% = 48 000

Monthly depreciation: 48 000 / 12 = 4 000

Year 2:

Annual depreciation: (120 000 - 48 000) * 40% = 28 800

Monthly depreciation: 28 800 / 12 = 2 400

Year 3:

Annual depreciation: (120 000 - 48 000 - 28 800) * 40% = 17 280

Monthly depreciation: 17 280 / 12 = 1 440

Year 4:

Annual depreciation: (120 000 - 48 000 - 28 800 - 17 280) * 40% = 10 368

Monthly depreciation: 10 368 / 12 = 864

Year 5:

Annual depreciation: (120 000 - 48 000 - 28 800 - 17 280 - 10368) * 40% = 6 221

Monthly depreciation: 6 221 / 12 = 518.42

The asset continues to depreciate each year at 40% of its net book value at the start of that year.

Asset cost = 120 000

Depreciation percentage year 1 = 50%

Depreciation percentage year 2 = 60%

Depreciation percentage year 3 = 70%

Depreciation percentage year 4 = 80%

Depreciation percentage year 5 and subsequent years = 90%

Year 1:

Annual depreciation: 120 000 * 50% = 60 000

Monthly depreciation: 60 000 / 12 = 5 000

Year 2:

Annual depreciation: (120 000 - 60 000) * 60% = 36 000

Monthly depreciation: 36 000 / 12 = 3 000

Year 3:

Annual depreciation: (120 000 - 60 000 - 36 000) * 70% = 16 800

Monthly depreciation: 16 800 / 12 = 1 400

Year 4:

Annual depreciation: (120 000 - 60 000 - 36 000 - 16 800) * 80% = 5 760

Monthly depreciation: 5 760 / 12 = 480

Year 5:

Annual depreciation: (120 000 - 60 000 - 36 000 - 16 800 - 5 760) * 90% = 1 296

Monthly depreciation: 1 296 / 12 = 108

The asset continues to depreciate each year at 90% of its net book value at the start of that year.

Asset cost = 120 000

Number of periods EUL = 60

Monthly depreciation: 120 000 / 60 = 2 000

Annual depreciation: 2000 * 12 = 24 000

Asset cost = 120 000

Throughput EUL = 100 000 units

Statistical G/L code is 01-604090

The movements for Statistical G/L code 01-604090 are as follows:

| Periods | Year 1 | Year 2 |

|---|---|---|

| 1 | 1000 | 0 |

| 2 | 2000 | 0 |

| 3 | 3000 | 0 |

| 4 | 4000 | 0 |

| 5 | 5000 | 0 |

| 6 | 6000 | 0 |

| 7 | 7000 | 0 |

| 8 | 8000 | 0 |

| 9 | 9000 | 0 |

| 10 | 10000 | 0 |

| 11 | 11000 | 0 |

| 12 | 12000 | 22000 |

Year 1:

Monthly depreciation:

-

Period 1: 1000 / 100 000 * 120 000 = 1 200

-

Period 2: 2000 / 100 000 * 120 000 = 2 400

-

Period 3: 3000 / 100 000 * 120 000 = 3 600

-

Period 4: 4000 / 100 000 * 120 000 = 4 800

-

Period 5: 5000 / 100 000 * 120 000 = 6 000

-

Period 6: 6000 / 100 000 * 120 000 = 7 200

-

Period 7: 7000 / 100 000 * 120 000 = 8 400

-

Period 8: 8000 / 100 000 * 120 000 = 9 600

-

Period 9: 9000 / 100 000 * 120 000 = 10 800

-

Period 10: 10000 / 100 000 * 120 000 = 12 000

-

Period 11: 11000 / 100 000 * 120 000 = 13 200

-

Period 12: 12000 / 100 000 * 120 000 = 14 400

Annual depreciation: 93 600

Year 2:

Monthly depreciation:

-

Period 1 - 11: 0 / 100 000 * 120 000 = 0

-

Period 12: 22 000 / 100 000 * 120 000 = 26 400

Annual depreciation: 26 400

Asset cost = 120 000

Number of years EUL = 5

The sum of year digits is calculated as (1+2+3+4+5) = 15

Year 1:

Annual depreciation: 1 / (1+2+3+4+5) * 120 000 = 8 000

Monthly depreciation: 8 000 / 12 = 666.67

Year 2:

Annual depreciation: 2 / (1+2+3+4+5) * 120 000 = 16 000

Monthly depreciation: 16 000 / 12 = 1 333.33

Year 3:

Annual depreciation: 3 / (1+2+3+4+5) * 120 000 = 24 000

Monthly depreciation: 24 000 / 12 = 2 000.00

Year 4:

Annual depreciation: 4 / (1+2+3+4+5) * 120 000 = 32 000

Monthly depreciation: 32 000 / 12 = 2 666.67

Year 5:

Annual depreciation: 5 / (1+2+3+4+5) * 120 000 = 40 000

Monthly depreciation: 40 000 / 12 = 3 333.33

Asset cost = 120 000

At Year 1, the Number of periods EUL is 60 periods

At Year 4, the Remaining useful life is set to 36 periods (i.e. the Estimated useful life is now 72 periods and not 60 periods as it was in Year 1).

Monthly depreciation is calculated as: (cost on file - accumulated depreciation) / remaining life of asset in periods

Year 1

EUL = 60 periods, Cost = 120 000

Monthly depreciation: (120 000 - 0) / 60 = 2 000

Annual depreciation: 2000 * 12 = 24 000

Year 2

EUL = 48 periods, Depreciable Cost = 120 000 - 24 000 = 96 000

Monthly depreciation: (120 000 - 24 000) / 48 = 2 000

Annual depreciation: 2 000 * 12 = 24 000

Year 3

EUL = 36 periods, Depreciable Cost = 96 000 - 24 000 = 72 000

Monthly depreciation: (120 000 - 48 000) / 36 = 2 000

Annual depreciation: 2 000 * 12 = 24 000

Year 4:

At the beginning if Year 4, the EUL is changed from 24 periods to 36 periods. The total EUL of the asset is therefore increased to 72 periods (from the original 60 periods).

EUL = 36 periods, Depreciable Cost = 72 000 - 24 000 = 48 000

Monthly depreciation: 120 000 - (3 * 24 000) / (72 - (12 * 3) = 48 000 / 36 = 1 333.33

Annual depreciation: 12 * 1 333.33 = 15 999.96 = 16 000 rounded up

Year 5:

EUL = 24 periods, Depreciable Cost = 48 000 - 16 000 = 32 000

Monthly depreciation: 32 000 / 24 = 1 333.33

Annual depreciation: 12 * 1 333.33 = 15 999.96 = 16 000 rounded up

Year 6:

EUL = 12 periods, Depreciable Cost = 32 000 - 16 000 = 16 000

Monthly depreciation: 16 000 / 12 = 1 333.33

Annual depreciation: 12 * 1 333.33 = 16 000 (rounded up)

Depreciation is calculated using the declining balance and the straight line method. The greater depreciation value of the two methods is used.

Asset cost = 120 000

EUL = 5 years

Declining rate = 200%

Straight line rate = 20% pa (the asset's EUL is 5 years)

Year 1:

Declining balance calculation: 120 000 * (1/5 * 200%) = 48 000

Straight line calculation: 120 000 / 5 = 24 000

Annual depreciation: 48 000 (per declining balance calculation)

Monthly depreciation: 48 000 / 12 = 4 000

Year 2:

Declining balance calculation: (120 000 - 48 000) * (1/5 * 200%) = 28 800

Straight line calculation: 120 000 / 5 = 24 000

Annual depreciation: 28 800 (per declining balance calculation)

Monthly depreciation: 28 800 / 12 = 2 400

Year 3:

Declining balance calculation: (120 000 - 48 000 - 28 800) * (1/5 * 200%) = 17 280

Straight line calculation: 120 000 / 5 = 24 000

Annual depreciation: 24 000 (per straight line calculation as this is now greater than the declining balance calculation - i.e. 24 000 > 17 280)

Monthly depreciation: 24 000 / 12 = 2 000

Year 4:

Remaining book value is now 19 200 (i.e. Original cost minus all Accumulated depreciation to date)

Straight line depreciation is in use.

Annual depreciation = 19 200

Monthly depreciation: 19 200 / 12 = 1 600

Depreciation is calculated using the declining balance but no switch is made to the straight line method.

Asset cost = 120 000

EUL = 5 years

Declining rate = 200%

Year 1:

Declining balance calculation: 120 000 * (1/5 * 200%) = 48 000

Annual depreciation: 48 000

Monthly depreciation: 48 000 / 12 = 4 000

Year 2:

Declining balance calculation: (120 000 - 48 000) * (1/5 * 200%) = 28 800

Annual depreciation: 28 800

Monthly depreciation: 28 800 / 12 = 2 400

Year 3:

Declining balance calculation: (120 000 - 48 000 - 28 800) * (1/5 * 200%) = 17 280

Annual depreciation: 17 280

Monthly depreciation: 17 180 / 12 = 1 440

Year 4:

Declining balance calculation: (120 000 - 48 000 - 28 800 - 17 280) * (1/5 * 200%) = 10 368

Annual depreciation: 10 368

Monthly depreciation: 10 368 / 12 = 864

Year 5:

Declining balance calculation: (120 000 - 48 000 - 28 800 - 17 280 - 10 368) * (1/5 * 200%) = 6 220.80

Annual depreciation: 6 220.80

Monthly depreciation: 6 220.80 / 12 = 518.40

The asset continues to depreciate each year at (1/5 * 200%) of its net book value at the start of that year.

Asset cost = 1000

Half year rule calculation: 1000 * 20% / 12 / 2 = 8.34

Year 1:

Monthly depreciation from Period 2 onwards - 8.34

Year 2:

Monthly depreciation defaults to 20% - 16.67

| Periods | Year 1 | Year 2 |

|---|---|---|

| 1 | 0 | 16.67 |

| 2 | 8.34 | 16.67 |

| 3 | 8.34 | 16.67 |

| 4 | 8.34 | 16.67 |

| 5 | 8.34 | 16.67 |

| 6 | 8.34 | 16.67 |

| 7 | 8.34 | 0 |

| 8 | 8.34 | 0 |

| 9 | 8.34 | 0 |

| 10 | 8.34 | 0 |

| 11 | 8.34 | 0 |

| 12 | 8.34 | 0 |

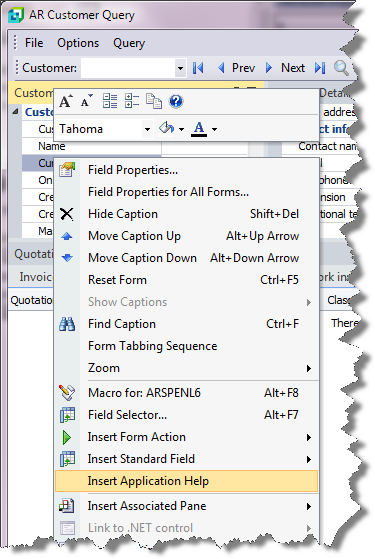

Inserting Application Help

You would typically follow this procedure to display help for the current program in a customized pane that can be pinned to the program window.

Information includes step-by-step instructions for the various functions available within the program, including a brief overview of what the program does, what setup options are required and how to personalize the program.

-

Open the program for which you want to insert application help into a customized pane.

This functionality is only available for a program that has panes.

-

Right-click any form field.

You can also click the triangle menu icon that appears in the title area of a pane.

-

Select Insert Application Help from the context-sensitive menu.

The application help appears in a pane within your program. You can reposition the pane using the docking stickers or pin it to the program window.

Removing the Application Help pane

If you no longer want to display application help in a pane for your current program, you can simply remove it.

-

Select the Close icon in the right-hand corner of the application help pane.

-

Confirm that you want to delete the pane.